What is National Pension Scheme (NPS)?

The National Pension Scheme scheme holds immense value for anyone who works in the private sector and requires a regular pension after retirement. The scheme is portable across jobs and locations, with tax benefits under Section 80C and Section 80CCD.

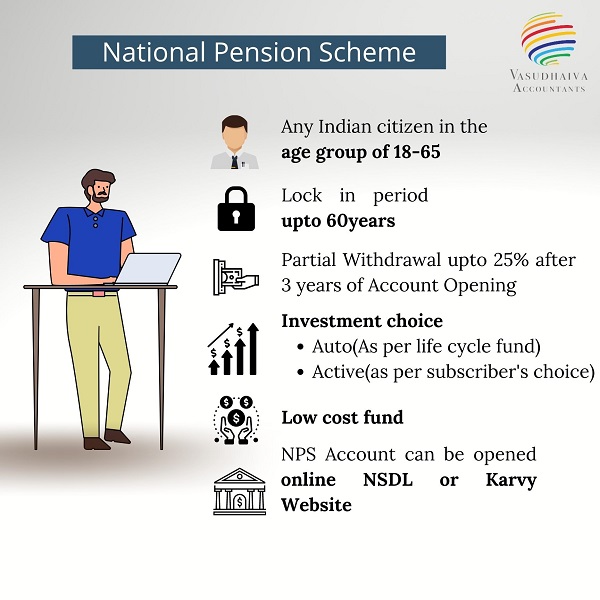

It is an initiative by the Central Government for social security. This pension programme is open to employees from the public, private and even the unorganised sectors except those from the armed forces.

The scheme encourages people to invest in a pension account at regular intervals during the course of their employment. As an NPS account holder, you will receive the remaining amount as a monthly pension post your retirement. After retirement, the subscribers can take out a certain percentage of the accumulated amount.

Earlier, the NPS scheme covered only the Central Government employees. Now, however, the PFRDA has made it open to all Indian citizens on a voluntary basis.

Who should invest in the NPS?

A regular pension (income) in your retirement years will be a boon, especially for those individuals who retire from private-sector jobs.

A systematic investment like this can make a massive difference to your life post-retirement. In fact, Salaried people who want to make the most of the Section 80C deductions can also consider this scheme.

The NPS is a good scheme for anyone who wants to plan for their retirement early on and has a low-risk appetite.

Features & Benefits of NPS

Returns/Interest

A part of the NPS goes to equities (this may not offer guaranteed returns). However, it offers returns that are much higher than other traditional tax-saving investments like the PPF.

This scheme has been in effect for over a decade, and so far has delivered 8% to 10% annualised returns. In NPS, you are also allowed the option to change your fund manager if you are not happy with the performance of the fund.

NPS tax benefit

- Tax Benefits on Investment

NPS subscribers can claim tax benefits on investment upto Rs. 1.5 lakh under section 80C of the Income Tax Act, 1961. The deduction comes under the overall upper limit of Rs. 1.5 lakh under section 80C.

- Tax Benefits on Returns

NPS returns are market linked and therefore returns depend on the performance on broader market performance. However, returns earned on NPS investments are entirely tax exempt.

- Tax Benefits on Maturity

NPS account matures at the age of 60. However, only 60% of the accumulated corpus can be withdrawn at the time of maturity. It is mandatory to invest rest 40% of the corpus in annuity.

Withdrawal Rules After 60

Contrary to common belief, you cannot withdraw the entire accumulated amount of the NPS scheme after your retirement. You are compulsorily required to keep aside at least 40% of the accumulated amount to receive a regular pension from a PFRDA-registered insurance firm and remaining 60% is tax-free.

Early Withdrawal and Exit rules

As a pension scheme, it is important to continue investing until the age of 60. However, if you have been investing for at least three years, you may withdraw up to 25% for certain purposes.

Purposes can include children’s wedding or higher studies, building/buying a house or medical treatment of self/family, among others. You can make a withdrawal up to three times (with a gap of five years) in the entire tenure.

These restrictions are only imposed on tier I accounts and not on tier II accounts. Please scroll down for more details on them.

Types of NPS Account

Tier I Account: This account carries a tax deduction under Section 80C up to Rs 1.5 lakh per annum and an additional amount up to Rs 50,000 per annum under Section 80CCD (1B).

- This is a non-withdrawable permanent retirement account. On maturity i.e at the age of 60, 60% of the accumulated amount which is tax-free can be withdrawn.

Tier II Account: This is a voluntary retirement-cum-savings account that can be opened only if you have a Tier I account. Subscribers are free to invest or withdraw their funds anytime according to their convenience. This account has no tax deductions, for private-sector employees or self-employed persons.

| Particulars | NPS Tier-I Account | NPS Tier-II Account |

| Status | Default | Voluntary |

| Withdrawals | Not permitted | Permitted |

| Tax exemption | Up to Rs 2 lakh p.a.(Under 80C and 80CCD) | 1.5 lakh for government employees Other employees-None |

| Minimum NPS contribution | Rs 500 or Rs 500 or Rs 1,000 p.a. | Rs 250 |

| Maximum NPS contribution | No limit | No limit |