House Rent allowance is for expenses related to rented accommodation.

If you don’t live in rented accommodation, this allowance is fully taxable.

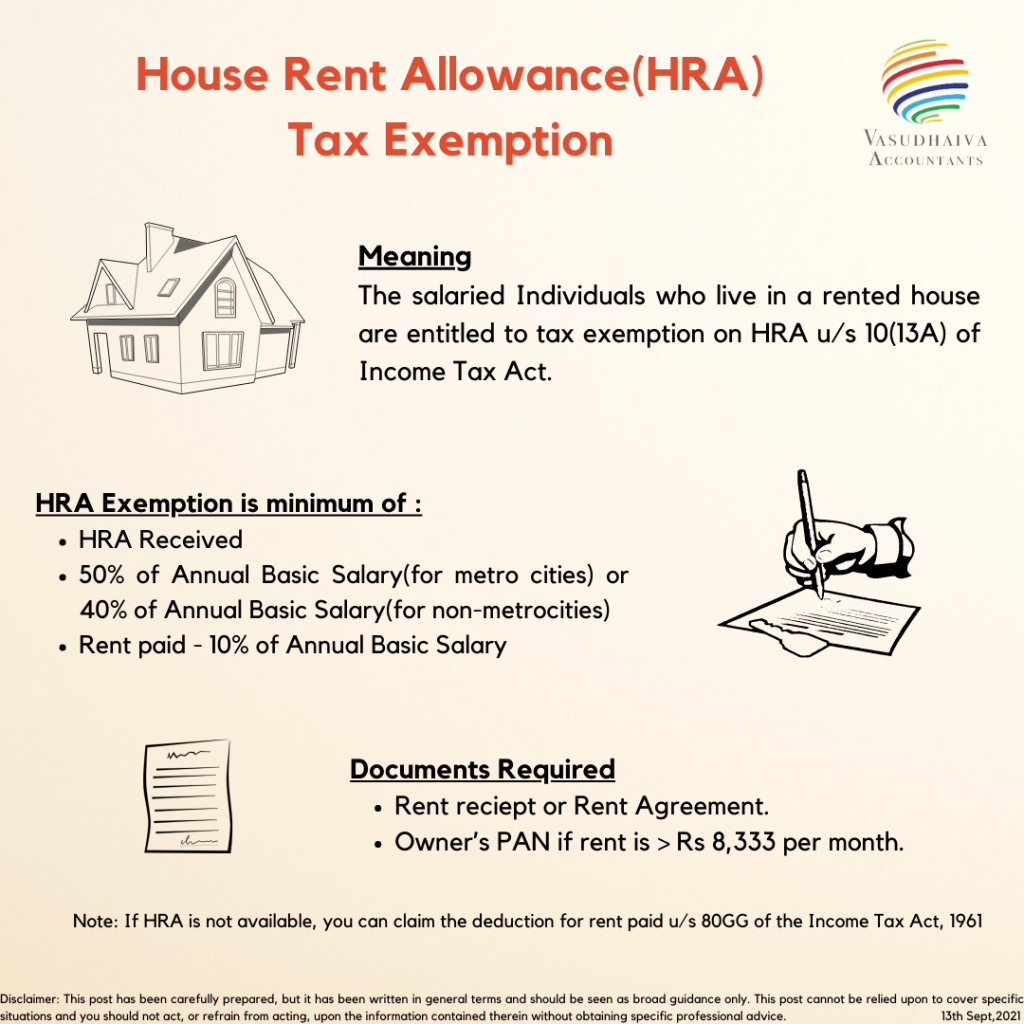

Salaried individuals, who live in rented houses, can claim the House Rent Allowance (HRA) to lower their taxes – partially or wholly.

HRA is one of the crucial components of an individual’s salary. It is the total amount employers pay employees towards their accommodation. The amount allotted towards HRA is tax deductible. Hence HRA calculation becomes important.

HRA calculation is based on a number of factors including the city of residence, the rent paid, and actual HRA received.

How is Tax Exemption from HRA Calculated?

The allowance available is the least of the following amounts:

- Actual HRA received

- 50% of [Basic salary + DA] for those living in metro cities

- 40% of [Basic salary + DA] for those living in non-metros

- Actual rent paid less 10% of basic salary + DA

DA – Dearness Allowance is a component of salary towards adjustment for cost of living paid generally to government employees, public sector employees, and pensioners. Dearness allowance is calculated as a percentage of basic salary to cover the impact of inflation.

Metro City is Delhi, Mumbai, Chennai, Kolkatta

Non Metro City- Other then metro city

What documents are required claiming HRA in ITR?

- Documents like rent receipts, and rent agreement will be required to be submitted to the employer for claiming deduction for house rent allowance.

- If the payment of rent is more than Rs 1 lakh per annum, then PAN of the house owner will be required to be submitted. On the basis of these proofs, employers would provide deduction for HRA in form 16.

Can HRA be claimed without proof?

Rent receipts are mandatorily required by the employer as a proof for claiming house rent allowance deduction.

What will happen if I miss to Submit proof or miss to claim HRA?

- If you have missed to submit the rent receipts and rent agreement to your employer at the time of proof submission, you can claim the HRA deduction while filing ITR.

- In case you miss to claim the HRA while filing a return, you can file a revised return to correct the error before the end of the assessment year.

Can HRA and Deduction on Home Loan Interest be claimed at the same time?

Yes, you may claim the HRA as it has no relation with your home loan interest deduction. Both can be claimed.

Employer doesn’t Provide with HRA?

If you do not receive HRA from your employer but are still actually paying rent then also you can claim the deduction under Section 80GG.

Following Conditions must be fulfilled to claim this deduction:

- You are self-employed or salaried

- You have not received HRA at any time during the year for which you are claiming

- You or your spouse or your minor child or HUF of which you are a member – do not own any residential accommodation at the place where you currently reside, perform duties of office, or employment or carry on business or profession.

In case you own any residential property at any place other than the place mentioned above, then you should not claim the benefit of that property as self-occupied. The other property would be deemed to be let out in order to claim the 80GG deduction.

How to Claim Deduction Under Section 80GG?

The least of following will be considered as the deduction under this section:

Rs 5,000 per month;

25% of adjusted total income*;

Actual Rent less 10% of adjusted total Income*

*Adjusted Total Income means Total Income Less long-term capital gain, short-term capital gain under section 111A and Income under section 115A or 115D and deductions 80C to 80U (except deduction under section 80GG).

Note Please note that the tax exemption of HRA is not available in case you choose the New tax regime. from FY 2020-21 (AY 2021-22)